Tired of slow, costly payments? AMINA Bank & Ripple just revolutionized EU cross-border transactions with Web3, slashing fees by 70%!#RipplePayments #Web3Finance #EUPayments

Quick Video Breakdown: This Blog Article

This video clearly explains this blog article.

Even if you don’t have time to read the text, you can quickly grasp the key points through this video. Please check it out!

If you find this video helpful, please follow the YouTube channel “MetaverseTrendsHub,” which delivers daily news.

https://www.youtube.com/@MetaverseTrendsHub

Read this article in your native language (10+ supported) 👉

[Read in your language]

AMINA Bank Partners with Ripple: Revolutionizing EU Cross-Border Payments in Web3

🎯 Difficulty: Enterprise

💎 Value Proposition: Faster Cross-Border Settlements, Reduced Costs, Enhanced Transparency via Blockchain

👍 Recommended For: Crypto Investors, DeFi Enthusiasts, Institutional Finance Professionals

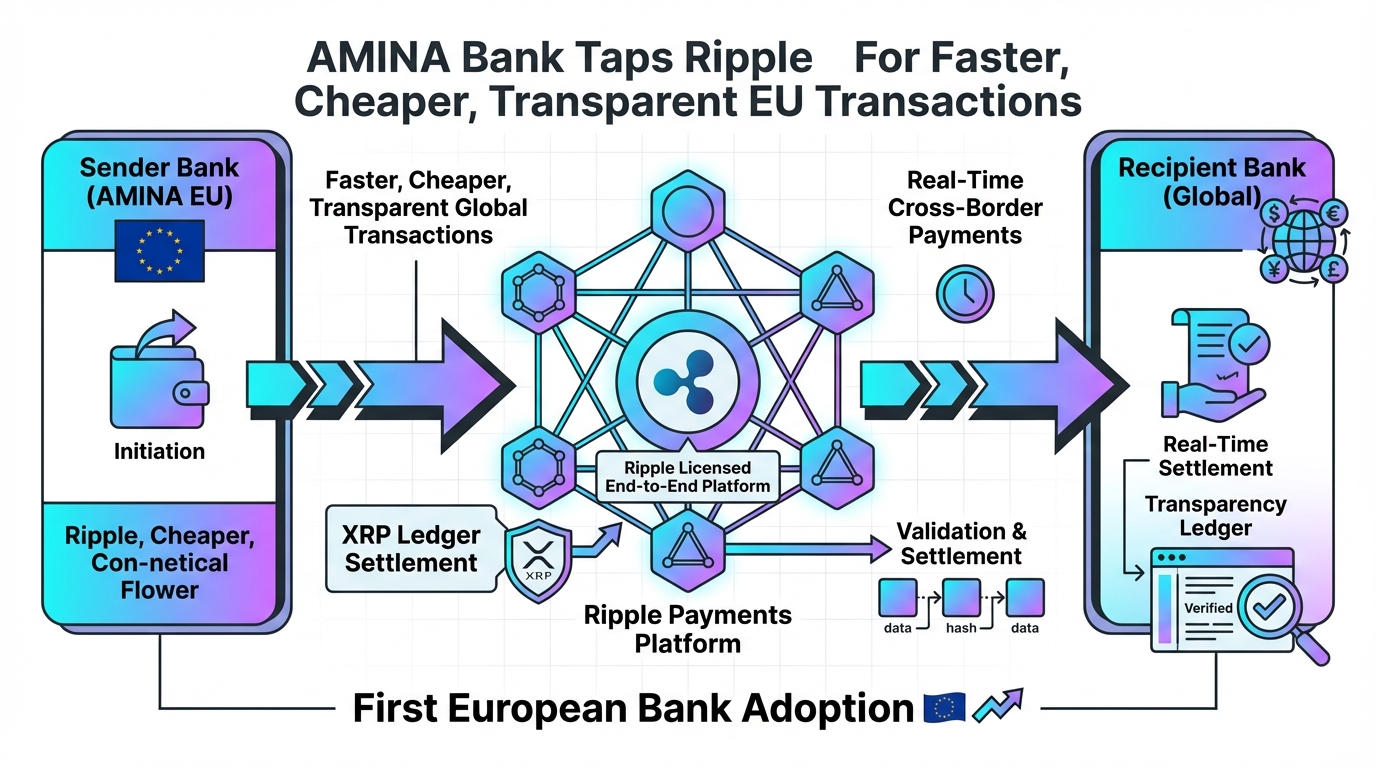

In the ever-evolving landscape of global finance, traditional cross-border payments have long been plagued by liquidity inefficiencies, high fees, and opaque processes. Enter Ripple’s latest milestone: a groundbreaking partnership with AMINA Bank, a FINMA-regulated Swiss institution, marking the first European bank to integrate Ripple Payments for near-instant, cost-effective transactions. As of recent web updates, this deal leverages Ripple’s blockchain rails to enable seamless fiat-to-stablecoin settlements, including the use of RLUSD stablecoin, positioning it as a game-changer for EU-based global trade. For investors eyeing “alpha” in utility-driven tokens like XRP, this signals stronger tokenomics through real-world adoption. To dive deeper into Ripple’s whitepaper and assess its decentralized payment protocols, tools like Genspark offer AI-powered analysis for thorough DYOR.

The Evolution: From Web2 Centralization to Web3 Decentralization

Let’s contrast the old guard with the new. In the centralized Web2 model, cross-border payments rely on intermediaries like SWIFT networks, where banks act as gatekeepers, charging hefty fees (often 1-3% per transaction) and delaying settlements for days due to batch processing and compliance checks. This creates friction in global commerce—think exporters waiting on funds while currencies fluctuate.

On the flip side, Web3’s decentralized model flips the script. Blockchain protocols like Ripple’s XRP Ledger use distributed ledgers for peer-to-peer validation, slashing intermediaries and enabling near-real-time TPS (transactions per second) of up to 1,500. Transparency is baked in via immutable records, reducing fraud risks. AMINA Bank’s integration exemplifies this shift, bridging traditional banking with crypto rails for cost savings of up to 70% on transactions, per recent reports from sources like Coinpaper and CryptoPotato.

For project teams looking to pitch such innovations, Gamma is invaluable for crafting visually stunning whitepapers or pitch decks that highlight these evolutions.

Core Mechanism: Technical Breakdown of Ripple’s Payment Rails

John: Alright, let’s cut through the hype—Ripple isn’t just another “to the moon” token; it’s a battle-tested protocol for institutional finance. At its core, the XRP Ledger employs a consensus mechanism called Ripple Protocol Consensus Algorithm (RPCA), which is neither proof-of-work nor proof-of-stake but a federated system where trusted validators (Unique Node List, or UNL) agree on transaction validity in seconds. This avoids the energy hogs of Bitcoin while achieving high throughput.

For AMINA Bank’s integration, Ripple Payments uses smart contract composability via the XRP Ledger’s hooks and the newly launched RLUSD stablecoin. Think of it as programmable money: transactions are atomic, meaning they either fully succeed or fail, ensuring no partial settlements. Developers can deploy this on compatible chains using tools like Ethers.js for integration or OpenZeppelin for secure contract audits, adhering to standards like ERC-20 for stablecoins.

Lila: To bridge for those new to this, imagine RPCA as a group of reliable friends voting on a dinner bill—quick and fair, without mining wars. In practice, AMINA taps into this for fiat on-ramps: a euro deposit converts to RLUSD via smart contracts, zips across borders on the ledger, and reconverts at the destination with minimal gas fees (XRP’s are fractions of a cent).

Tokenomics-wise, XRP serves as the bridge asset, with a fixed supply of 100 billion (45% in circulation), designed for low volatility and high utility. ROI potential? Recent whale accumulation and South Korean trading interest, as noted in Cryptopolitan, suggest upward pressure on XRP’s price, especially with EU adoption boosting TVL (total value locked) in Ripple’s ecosystem.

Use Cases: Real-World Applications in Metaverse and Blockchain

First, for global remittances: A freelancer in the EU Metaverse economy—say, designing virtual assets—can receive payments from a U.S. client instantly via AMINA’s Ripple setup, bypassing SWIFT’s delays and fees. This enhances liquidity in decentralized marketplaces.

Second, in supply chain finance: An EU exporter using blockchain oracles (integrated via tools like Chainlink) can trigger automatic payments upon delivery verification, with Ripple ensuring transparent, auditable trails. Investors see “alpha” here through tokenized invoices yielding APYs of 5-10% in DeFi pools.

Third, institutional DeFi: Banks like AMINA can offer yield farming on stablecoin deposits, where users stake RLUSD in protocols for governance tokens, decentralizing control while complying with regs. For NFT/GameFi projects promoting such use cases, Revid.ai is perfect for creating teaser videos. And if you’re building these dApps, check out Nolang for interactive Solidity coding lessons.

| Aspect | Traditional Web2 App (e.g., SWIFT) | Web3 dApp Solution (e.g., Ripple with AMINA) |

|---|---|---|

| Speed | Days for settlement | Near-instant (seconds) |

| Cost | High fees (1-3%) | Low fees (fractions of a cent) |

| Transparency | Opaque, intermediary-dependent | Immutable blockchain ledger |

| Decentralization | Centralized control | Distributed validators |

Conclusion: Seize the Opportunity in Web3 Finance

This AMINA-Ripple partnership isn’t just news—it’s a blueprint for Web3’s infiltration into traditional finance, promising ROI through enhanced utility and adoption. With XRP potentially rebounding above $2 amid whale activity, now’s the time to explore. Start by setting up a non-custodial wallet like MetaMask, bridge assets via official Ripple tools, and join related DAOs for governance input. For automating crypto alerts or Discord ops, Make.com streamlines it all. Dive in, but remember: DYOR and manage risks.

👨💻 Author: SnowJon (Web3 & AI Practitioner / Investor)

A researcher who leverages knowledge gained from the University of Tokyo Blockchain Innovation Program to share practical insights on Web3 and AI technologies. While working as a salaried professional, he operates 8 blog media outlets, 9 YouTube channels, and over 10 social media accounts, while actively investing in cryptocurrency and AI projects.

His motto is to translate complex technologies into forms that anyone can use, fusing academic knowledge with practical experience.

*This article utilizes AI for drafting and structuring, but all technical verification and final editing are performed by the human author.

🛑 Disclaimer (NFA)

Not Financial Advice. Content is for educational purposes only. Cryptocurrency and NFT investments carry high risks. DYOR (Do Your Own Research).

This article contains affiliate links.

▼ Recommended Web3 x AI Tools

References & Further Reading

- Ripple Makes European Banking History With AMINA Bank Deal

- AMINA Bank Becomes First in Europe to Go Live With Ripple Payments

- Ripple Secures Breakthrough Banking Adoption in Europe: Details

- AMINA Bank Taps Ripple To Deliver Faster, Cheaper, And Transparent Global Transactions In EU